Turning Point: Interest Rates Increase

When the Feds started raising interest rates, together with the world’s central banks in an effort coordinated by Bank for International Settlements (also known as, the central bank of central banks), a few things started to change for Silicon Valley Bank.

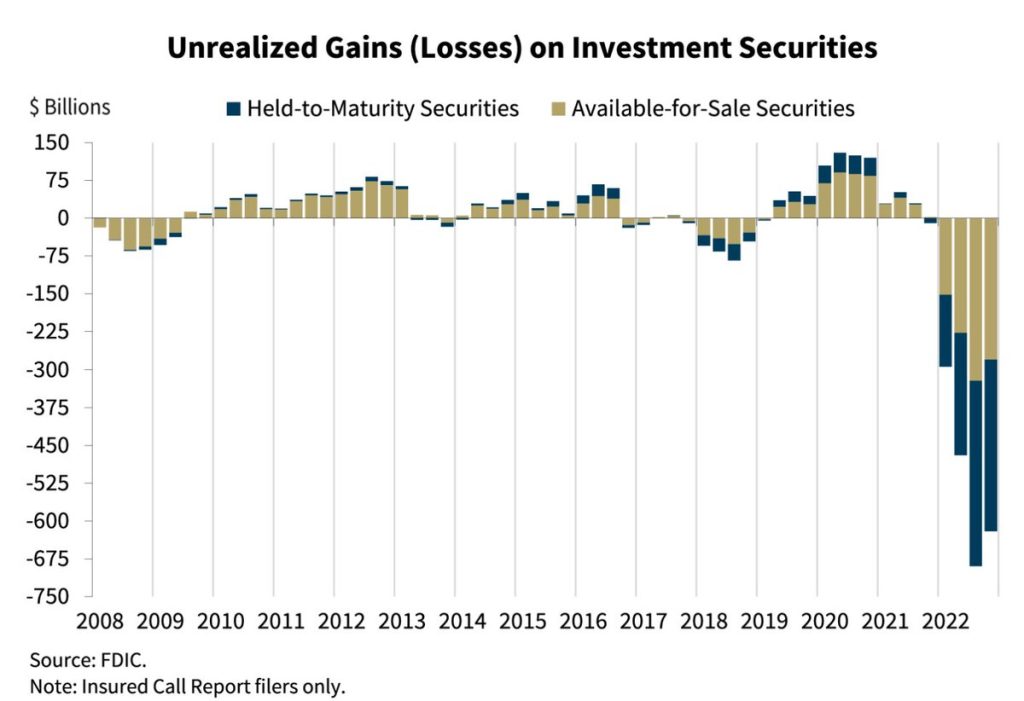

Unrealized Losses

Like explained above, when interest rates rise, the value of fixed-income securities bought at low interest rates decreases. And fast.

Silicon Valley Bank had a total of $ 120 billion bond portfolio on the mid-curve. That means that most of their securities would mature in 5 years. According to my calculations, for every 0,10% rise in interest rates, their portfolio would book a total unrealized loss of $ 576 million.

Note: it is technically called unrealized loss, because you lose money only if you are forced to sell. But in the meantime, from accounting perspective, those products “lost value”.

Anyways, with interest rate raising a 2,00% (on average), Silicon Valley Bank booked a total of $ 14 billion unrealized losses, equal to their entire equity capital.

One important thing to mention here is that all those fixed-income securities were not hedged! In other words, Silicon Valley Bank had not insured any of their fixed-income products

PS: and in all this, none of the rating agencies and regulators found this suspicious!

Why Was Their Portfolio Not Insured

For those of you not familiar with fixed-income securities, here’s what you need to know about this.

Imagine you have build up a position in hedged fixed-income securities at low interest rates. When interest rate rise, your bonds will lose value, but your hedge will increase in value. In a rising interest rate market, hedging positions bought at low-interest rates appreciate in value.

The opposite is true in decreasing interest rate markets. When interest rate are lowered compared to your fixed-interest products, your bonds will increase in value, your hedge will decrease instead.

However, here is an important difference. A increase or decrease in your securities price will be booked in your balance sheet. On the other hand, an increase or decrease in your hedging component will end up in your profit and loss statement!

So what those banks were doing by not hedging their portfolio was to protect their profit and loss statement… on the short-term. Why? Well, guess how bonuses are calculated at the end of the year 😮💨

Fewer Funds Flowing To Startups

Generally, when interest rates increase, investors tend to be satisfied with less returns if that means less risk. While in markets a low interest rates, investors tend to take more risk in the hope of realizing higher returns.

This means that the risk/return ration in startup investing was less attractive to investors than traditional financial products such as treasury bonds. Throughout 2022, lending money to the government would pay between 2-4% a year, depending on the maturity. This is what is typically called “risk-free”.

This resulted in a decrease in deposits in Silicon Valley Banks due to fewer capital available for the startup space.

No comment yet, add your voice below!