Genesis Bankruptcy: A Ticking Bomb In The Crypto World

Digital Currency Group, Genesis, Gemini, Grayscale, Three Arrow Capital… these names have been all over the crypto news lately for what it might be one of the largest crypto schemes far. A potential fall of these institutions will have massive consequences on the Bitcoin prices and the entire crypto ecosystem.

All the companies mentioned above are part of the Digital Currency Group (DCG), a large holding company in the crypto space founded by Barry Silbert: former banker and one of the crypto OGs. Some of the most well know companies under the holding are:

- Bitcoin’s institutional trust Grayscale,

- crypto news channel CoinDesk (publisher of the famous article on FTX and Alameda on November 2, 2022),

- trading company Genesis, and

- Bitcoin’s mining pool Foundry.

However, the list does not end here. DCG has their hands in many ventures in the crypto space, being one of the earlier investors in blockchain technology. After latest events though, it might be more appropriate to rebrand to Digital Con Group. Why? Well, you will see. The plot is about to get thicker.

The scheme I am about to unravel has been running for quite some years, with many investors being unaware of it. Thanks to the collapse of FTX, the whole thing started to wobble, exposing the whole scheme.

After all, quoting one of my favorite investors: “Only when the tide goes out do you discover who has been swimming naked”.

Who Was Involved In The Bankruptcy S#itshow

Before we dive into the actual scheme, let’s take a look at the actors in this theatrical crypto play. In order of relevance: Grayscale, Genesis, Three Arrow Capital, Gemini.

Grayscale

As mentioned above, Grayscale is one of the most notorious digital asset managers. The company was founded in 2013, launching a Bitcoin trust fund. By doing so, Grayscale offered institutional investors a way to invest in Bitcoin indirectly by buying shares of their trust, called GBTC (Grayscale’s Bitcoin Trust). This was (and to some extent still is) the only was institutional investors could get exposure to Bitcoin through a regulated company.

Genesis

Genesis, on the other hand, is a broker in the crypto market. Their primary business consists in trading, custody, and most importantly for this story lending and borrowing. Most of Genesis’s clients were hedge funds and other trading companies using their lending platform to leverage their position.

Three Arrow Capital

Amongst Genesis’s clients, a famous name in the crypto market: Three Arrow Capital (3AC). 3AC went bust in June 2022, as a consequence of the Terra/Luna collapse.

3AC had a large account on Genesis. Their position was about $2,36 billion. These were crypto assets borrowed on the Genesis platform. 3AC’s position was supposedly undercollateralized. So when they went bust in June 2022, this put Genesis in a very dangerous position.

Gemini

Another of Genesis’s clients worth mentioning in this story is Gemini. Gemini is a (centralized) crypto exchange founded by the Winkelvoss brothers. Gemini became known in the market as the first (and only to this date I believe) to get a full license to operate in the state of New York. The state is famous for their strict financial regulations. Most of the classic crypto exchanges are not available for New York residents. Gemini was also known for their campaigns in the New York State bragging to be one of the only decent (regulated) exchange in the crypto space.

Despite the well-managed license application with New Yorkers authorities, Gemini messed one thing up BIG time. In February 2021, they launched a staking program for their customers. The customers could lend out their cryptos and generate passive income. Easy, right? It was actually. All the customers had to do was turn on a setting called “Staking” and their position would be lent out. However, Gemini did not do this themselves. The lending was done through Genesis. Gemini would act as an agent for Genesis in exchange for a cut of the interest generated by lending their customers’ position. Not long after the launch, Gemini collected a total of $900 million from about 350.000 of their customers.

The Creativity of Capital Markets

The fun starts with Grayscale’s Bitcoin Trust: GBTC. For many years, GBTC shares were the only way institutions could invest in Bitcoin, albeit indirectly.

GBTC was set up in a very simple way. They held Bitcoins in the trust while investors could buy shares of the trust. For every 1 BTC, investors would get 1000 GBTC shares. So in other words 1 GBTC = 0,001 BTC.

However, we live in a free market. The GBTC shares can also be bought and sold on the secondary market. This means that the price of those shares could vary from the price of the underlying asset: BTC. This simply based on the demand for such shares from institutional investors.

This creates what became known as the GBTC premium or discount. Premium, when GBTC would trade at a price point higher than Bitcoin. Discount, the opposite.

Earning The GBTC Premium

Typically GBTC would trade at a premium compared to Bitcoin’s net asset value (NAV). The premium reached peaks as high as 130% in periods of high demand for GBTC shares (for example in 2017). Little spoiler: notice how the premium turns negative somewhere in January 2021. Keep that date in mind. This is an important turning pointing this whole story.

The premium, however, was not easy to arbitrage since GBTC could only be converted in Bitcoins during designated periods of time when they would be unlocked. The challenge of arbitraging the GBTC premium intrigued a number of investment funds and traders worldwide. Among them, Three Arrows Capital who took it to a whole new level. After all, returns could be pretty high, especially when leveraging your position.

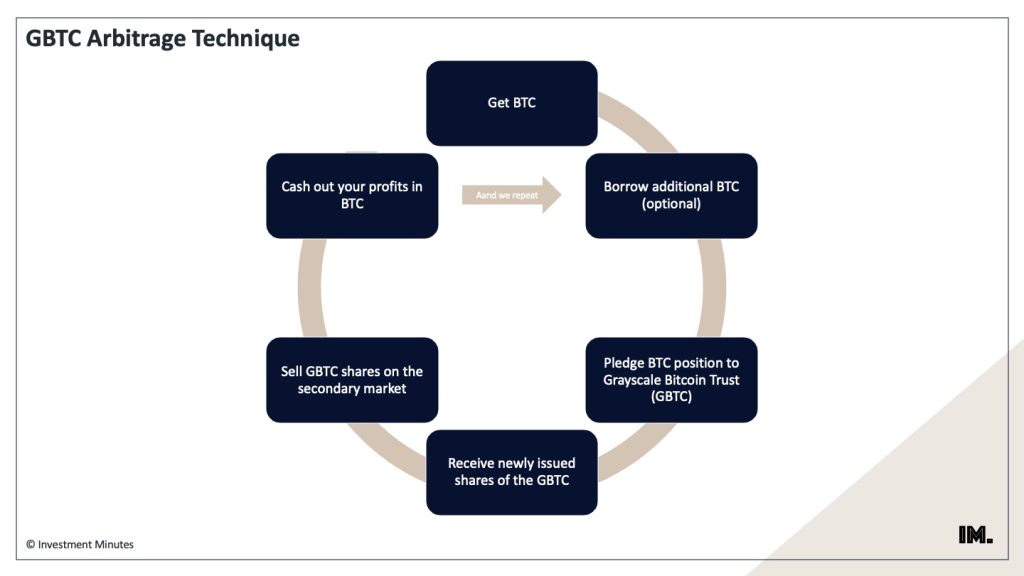

GBTC Arbitrage Technique

Here is how it worked. Traders would borrow BTC and make a commitment in-kind to Grayscale’s Bitcoin Trust. In return for that commitment, the traders would get GBTC shares. These shares would be traded (after their vesting period) on the public market at a premium compared to the Bitcoin’s value initially commitment to the fund.

Assuming GBTC traded at a premium, this technique would help inflate the value of GBTC further. This, in turn, would stimulate more borrowing and in-kind commitments to the fund to further fuel the self-reinforcing cycle.

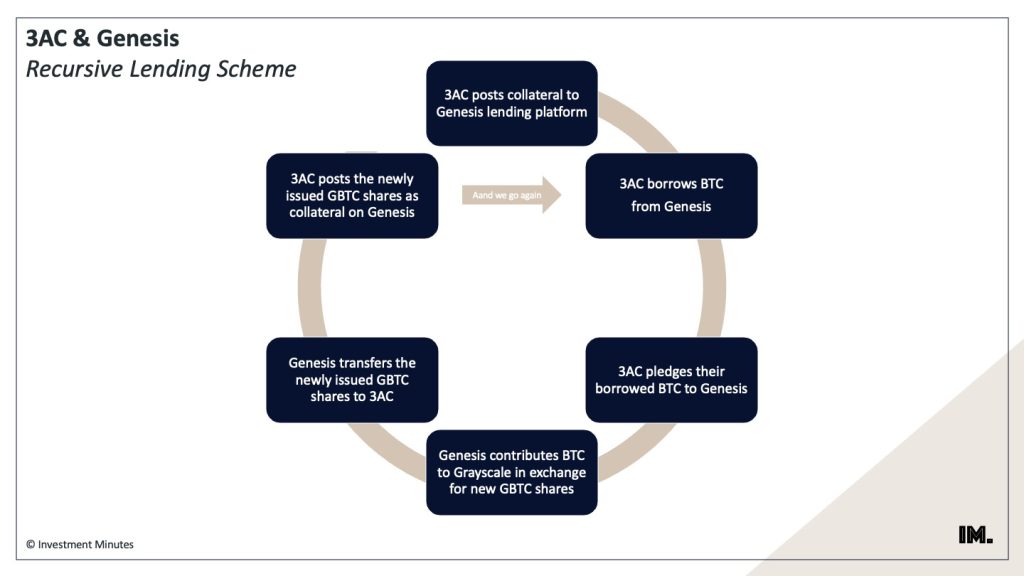

How 3AC and Genesis Earned The GBTC Premium

3AC started playing this exact game using Genesis as their platform to borrow BTC to leverage their position.

In particular, 3AC would post some collateral to Genesis in order to borrow BTC. BTC was then sent back to Genesis to issue new GBTC shares. This was possible because Genesis was an authorized participant in Grayscale. Once GBTC shared were issued, but still vested, they would be posted on Genesis as a collateral to borrow even more. And the cycle repeated.

How The Cycle Breaks

So far, however, we are talking about trading risk. These types of techniques are rather normal in the trading world. Also in the traditional financial system. They typically are okay as long as (little disclaimer here):

- the collateral used for the loans is reasonable for the risk being run by the lender,

- there is no artificial value inflation created deliberately by the asset owners.

3AC’s Collateral… Damage

The trading technique would collapse if GBTC would trade at a discount compared to Bitcoin value. This was no secret to anyone. Genesis seemed to be fully aware of the limitation of this model. In their quarterly report in early 2022 they write:

“Traders who previously borrowed BTC to contribute in-kind private placements to the trust, with the intent to sell at a premium in the public market after the vesting period, lost the ability to arbitrage the spread.”

As a result, those who had borrowed and pledged their BTC in return for GBTC were in a squeeze. One of them was obviously 3AC.

What I find really interesting is that after the inflection point somewhere in February 2021, Genesis kept lending to 3AC. This was happening despite 3AC not being able to pledge those BTC for new GTBC shares. As you can see, the GTBC share amount remains constant after the inflection point in 2021 Q1, when GTBC started trading at a discount to BTC value.

As a result of this, Genesis’s collateral was getting thinner and thinner. Once again, despite this, the lending continues, possibly because they thought they might have a chance to recover (yet to be incurred) losses if they could hold just long enough until the trend would invert.

Also, Genesis never disclosed this position. There was a short-term benefit into all this, in that the GBTC collateral was being kept from the open market in the hope to manage the sell pressure on the shares and thus the discount. Something that did not manifest for Genesis, as the GBTC discount kept increasing after that.

Period | GBTC/BTC (End of quarter) | GBTC Shares (Millions) | BTC Outstanding | Collateral (%) |

|---|---|---|---|---|

2020 Q1 | +18,09% | 316 | 45.162 | 14% |

2020 Q2 | +10,32% | 403 | 79.403 | 20% |

2020 Q3 | +10,31% | 471 | 80.246 | 17% |

2020 Q4 | +23,52% | 639 | 71.018 | 11% |

2021 Q1 | -8,34% | 692 | 65.619 | 9% |

2021 Q2 | -6,94% | 692 | 100.197 | 14% |

2021 Q3 | -16,89% | 692 | 82.126 | 12% |

2021 Q4 | -22,04% | 692 | 74.246 | 11% |

2022 Q1 | -27,77% | 692 | 92.015 | 13% |

How DCG Was Involved

Where it gets dodgy here is when we look at the involvement of the mother company DCG. Remember, they owned both Grayscale and Genesis. If DCG was involved, this would officially classify as a Daisy Chain.

A Daisy Chain is a fraudulent scheme where a group of investors deliberately works together to engage in a scheme to artificially increase the value of the financial product. Talks of such a fraudulent scheme were already spreading on Twitter in July 2022, after this thread below by Data Finnovation and extended article.

Amazing similarities between 3AC sales of GBTC and DCG purchases:

– 3AC accumulated position while, simultaneously, pledging the shares to Genesis

– DCG started buying

– DCG’s buys match 3AC’s unpledged amount that somehow was sold

WTF— Data Finnovation (@DataFinnovation) July 22, 2022

Bankruptcy, Recapitalisation, and Creative Accounting

The hopes were crushed when 3AC went under and with them the collateral Genesis was holding. This left Genesis with a gap in their balance sheet estimated at $1,2 billion.

At this point Genesis had two options:

- restructure the balance sheet, or

- recapitalize to fill the $1,2 billion gap.

This is when DCG came in and used some creative accounting tricks to buy time and hold long enough awaiting the discount to turn into a premium again.

DCG issued a promissory note to Genesis worth $1,2 billion. A promissory note is a loan to the company. The note had a term of 10 years at an interest of 1%. The interesting this is that this promissory note was accounted for as current assets by Genesis, thus “filling the gap” on their balance sheet.

And The Tide Goes Down

Despite their creativity, there is a few issued with what DCG and Genesis arranged. And here is my problem with that.

- Arm-length’s Transaction – With an interest of 1% on a 10-year unsecured note, this is clearly a sign of a mother company taking the risk to try and save one of the daughter companies. A commercial rate on such a debt obligation should be at least 10 times higher. Imagine that the rate at which European countries can lend from the ECB is almost 2,5 higher!

- Note Liquidity – Given that the note is purely a mother-to-daughter company shift in liability, there is no way on Earth that the note can be counted as current assets!

For those of you who might not know, current assets are company’s assets that can be sold for cash within 1 year. These are typically cash equivalents in other words, as in assets can that be easily sold when the company is in need for cash.

Again, there is no way that promissory note can be sold on the bond secondary market at face value for $1,2 billion.

The only reasonable way to solve this issue was if DCG had $1,2 billion in current assets they could use for Genesis’s balance sheet gap. But that is not the case!

After FTX collapse, there was no doubt this temporary fix was a scam. The tide goes down, and it turned out DCG and Genesis they had been swimming naked after all.

My Final Thoughts

This story is by far not over yet. The Securities and Exchange Commission (SEC) as well as the Department of Justice (DOJ) are investigating suspecting a Daisy Chain.

In the meantime DCG is trying to raise capital in any way they can to the extent that they put their entire venture portfolio with $3 billion up for sale. This is obviously bad news for those projects with ripple effects onto the entire market.

As for Gemini, it is not sure what the impact will be. After all, clients have lost funds, withdrawals are suspended, and they will have to deal with both reputation and legal consequences in the coming months. The same holds for Bitvavo. Their involvement in the lending scheme is not clear. They did offer a staking program for customers, so chances are they were also providing liquidity for 3AC or Genesis to arbitrage GBTC.

The biggest question to me is what will happen to Grayscale. GBTC shares are still 30% below Bitcoin’s value. Grayscale’s effort to convert the fund into an EFT has been rejected by the SEC thus killing their hope to attract retail money for new liquidity.

The issue is that if DCG were to go bankrupt, the majority of their BTC would be sold in the market with massive consequences for Bitcoin, Bitcoin’s ecosystem, and the entire crypto market.

Newsletter

Stay up-to-date with the latest developments in the stock and crypto market., fund, and crypto market.

Disclosure

These are unqualified opinions, and this newsletter, is meant for informational purposes only. It is not meant to serve as investment advice. Please consult with your investment, tax, or legal advisor, and do your own research.

No comment yet, add your voice below!