Why do we need regulations in the crypto market?

In many of my articles, I talked about the three keys to the future success of the crypto ecosystem. One of the three is: INSTITUTIONAL ACCEPTANCE. This means banks, wealth managers, investment and pension funds start “parking” some of their money into crypto assets.

This will not just happen out of their good hearts. For large institutional money to flow in any asset, we need a clear (amongst other things) a clear regulatory framework. This crypto regulatory framework is just a rule book spelling out the rules of the game for investors and issuers of crypto assets alike. No more than that.

Bank associations, central banks, governments have danced around the topic of crypto regulations for a while by now. And honestly, we are not even close to having half a decent framework in place for a pension fund to even consider investing in crypto. The interest is there. You can read it everywhere. Just see how much coverage the collaboration between Coinbase and Blackrock got even in mainstream media. But from interest to actual investments… that will take some time still, I’m afraid.

The First Attempt At A Worldwide Crypto Regulation

The first attempt at a decent global crypto regulation is coming from the Bank for International Settlements, also known as BIS. The framework will regulate the exposure banks can have in various crypto assets.

The BIS is the central bank of central banks, working with almost all central banks in the world. Recently, the BIS has been heavily involved in the development of central bank digital currencies (CBCD). This is a matter of control, as who holds the control over how you can manage your funds – governments or you.

The BIS have now finalized the standards for crypto custody, which will be effective as of 2025. These standards have 2 categories of crypto assets and 4 key components ultimately determining:

- The maximum exposure an institution can have in a certain crypto asset, and

- The additional capital they need to hold as collateral for that position, or in other words: the capital requirements.

For those of you who are interested, you can read the full proposal here.

Group 1 Assets

Group 1 Assets are any coin or tokens that are analogous to existing assets.

In other words, any digital form of shares, debt obligations, stock certificates is considered a Group 1 Asset. These assets are further split into two sub-category: 1A) for all traditional financial assets, and 1B) for centralized stable coins.

Note that algorithmic stable coins are not part of Group 1B. This is not very prominent in the proposal. I found this hidden in a footnote. But the implications are huge.

For all Group 1 Assets, the BIS treats the digital coins or tokens as if they were traditional financial assets. There is therefore no specific maximum exposure, nor additional capital requirements.

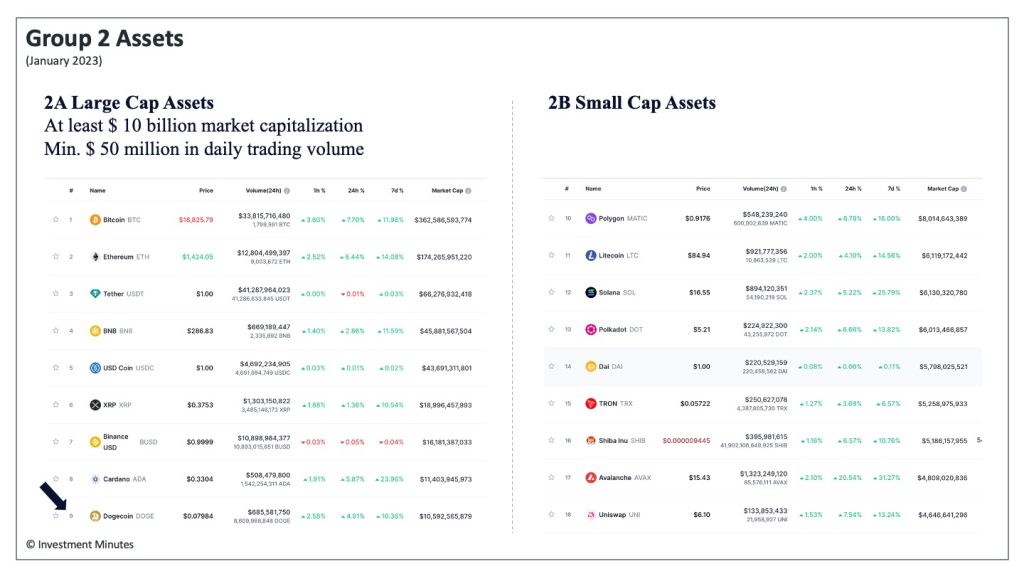

Group 2 Assets

Group 2 Assets are crypto or tokens that are not analogous to traditional financial assets.

Group 2 includes algorithmic stable coins and unbacked crypto assets such as BTC, ETH, and so on. Group 2 Assets are further split into two sub-categories: 2A) large cap, and 2B) small cap.

Group 2A Large Cap Assets are coins or tokens with a minimum market capitalization of $10 billion and a daily trading volume of $50 million (10% trimmed mean). If we take a snapshot of the current crypto market, Group 2A would include all the top 10 crypto projects.

Funny enough, DOGE is currently at $10,5 billion market cap, that is enough to get a Group 2A label.

This means bank could technically hold DOGE! This goes to show that there is still work to do on this framework

4 Key Component of the BIS Crypto Regulation Proposal

Here are the 4 key components of the BIS proposal to determine exposure limits and capital requirements:

- Group 2 Exposure Limits

- Infrastructure Risk

- Redemption Risk

- Additional Risk Elements

Group 2 Exposure Limits

If an institution wants to invest in a Group 2 Asset, the BIS sets the maximum exposure to 2% of the bank’s Tier 1 capital.

Help Line

What is Tier 1 capital, or Additional Tier 1 capital (AT1)? AT1 is a specific capital requirements banks need to hold in cash. They are bonds issued by banks that contribute to the total level of capital they are required to hold by regulators. Tier 1 capital ratio has to be at least 6% of total deposits and assets, even more for those institutions that are “too big to fail”.

Both exposure and capital requirements depend on the Group 2 sub-category. For Group 2A Large Cap Assets, banks can go up to 2% exposure while holding 100% reserve of the net asset value. For Group 2B Small Cap Assets, 1% and a capital requirement of 12,5x!

NB: which such a capital requirement on small cap projects, BIS is actually heavily discouraging investments into small crypto assets.

Infrastructure Risk

Infrastructure risk is an additional risk due to the network the coins exist on. Redemption risk applies only to coins being kept on balance sheets, and before adding any coin to their balance sheets, central banks must check whether the issuer is sufficiently regulated and if it can redeem withdrawal requests.

An infrastructure risk add-on of 2,5% has been set, meaning that if a central bank has 100 million USDC, this would count as 102,5 million USDC. This is supposed to ensure a sort of hedging against the network the coin is implemented on. A redemption risk component has been added, replacing the basis test with additional regulatory requirements (MiCA).

Redemption Risk

Before adding any coin to their balance sheets, banks must check whether the issuer is sufficiently regulated and the extent to which they can redeem withdrawal requests.

Based on the available liquidity, the bank can decide to increase the add-on for redemption risk. This means that the real allocation will be even lower than the ideal 2%.

I bet this was added after the FTX collapse. Just a wild guess.

Additional Risk Elements

This is a wide category requiring additional cautionary measures on liquidity, leverage, and other risk-factors the bank is exposed to.

What I Think Of The BIS Framework

Getting straight to the point, I think this framework is very bullish for the crypto ecosystem. Institutional acceptance is a catalyser for more maturity and standardization in the market.

However, the form in which the crypto ecosystem will evolve as a result of the large institutional acceptance is not yet clear to me. There is basically two extremes: fully decentralized and completely centralized. The good old battle between crypto fundamentalists and government organization. Between stable coins and central bank digital currencies.

I believe that the two world will coexist. Some parts of the infrastructure will be fully decentralized. Others will be run by government organization leveraging blockchain infrastructure where I can connect to even with my cold-storage private wallet.

Another simple observation of this more hybrid model is that not all central banks are in a position to design, implement, and run their own CBDC. These are more likely to make use of a stable coin launched on one of the main networks (e.g., Bitcoin, Ethereum).

The Ultimate Middle Point

Although crypto fundamentalist will tell you that central banks acquiring classic stable coins is the end of the crypto ecosystem as we know it. This comment is based on the assumption that such a big holder of stable coins on one single network will have so much voting power on the network to create a natural bias in the network. But, I do see a way forward without compromising the ecosystem: governance. Governance protocols are the key to future stable coins that can handle large institutional positions while ensuring the network can still run its operation in a fair way for all stakeholders. Beware: the protocol might even be fully algorithmic! Even better, if you ask me. Than all the human biases are out.

Newsletter

Stay up-to-date with the latest developments in the stock and crypto market., fund, and crypto market.

Disclosure

These are unqualified opinions, and this newsletter, is meant for informational purposes only. It is not meant to serve as investment advice. Please consult with your investment, tax, or legal advisor, and do your own research.

No comment yet, add your voice below!